My friend Edward Siedle, a former SEC attorney who has been involved in many ERISA suits was giving a training to DOL attorneys and regulators a few years back. A DOL staffer asked Siedle who polices “Prohibited Transactions,” and Siedle answered you (the DOL) do. The entire room of DOL staffers replied that we do not, we thought outsiders did. So basically, for the last 5 decades, no one has policed prohibited transactions. The industry has lobbied for exemptions, but upon scrutiny, most do not hold up with many products.

The Industry has become deadly fearful of prohibited transactions cases enabled by Cunningham v. Cornell, as they are in a desperate struggle to put in legislation to weaken ERISA https://commonsense401kproject.com/2025/11/29/rep-randy-fine-files-bill-to-force-private-equity-annuities-and-crypto-into-401ks/ to keep it from starting. The Plaintiff bar has in general been slow to adapt because they are mostly focusing on the top 500 largest plans, where it is easier to find plaintiffs and they think they can find easier $$$$.

How to Find ERISA Prohibited Transactions Using the IRS/DOL Form 5500

One of the most misunderstood facts in ERISA litigation is this:

Many prohibited transactions are disclosed by defendants themselves — on the IRS/DOL Form 5500.

The Form 5500 is not confidential. It is a public record, filed annually with the IRS, Department of Labor, and PBGC, and it often contains everything a regulator, journalist, or plaintiff attorney needs to identify conflicted compensation arrangements. It is easily accessible on the web at https://www.efast.dol.gov/5500Search/

Below is a practical guide to finding prohibited transactions using nothing more than the Form 5500—illustrated with the Lakeshore Learning Materials 401(k) Plan (2024) filing.

I. What Is the Form 5500—and Why It Matters

Form 5500 is the Annual Return/Report of Employee Benefit Plan, required under ERISA §§104 and 4065 and the Internal Revenue Code.

Key points:

It is signed under penalty of perjury

It is open to public inspection

It requires affirmative disclosure of:

Service providers

Compensation

Indirect compensation

Party-in-interest relationships

Insurance contracts and collective trusts

This makes the Form 5500 one of the most powerful—and underused—tools for identifying ERISA prohibited transactions.

(Page 1 of the filing confirms this plan is a single-employer ERISA plan and that the Form is open to public inspection

LakeshoreSelect24

)

II. Step One: Go Straight to Schedule C (Compensation)

Schedule C is where prohibited transactions often reveal themselves.

A. What Schedule C Discloses

Schedule C requires disclosure of:

All service providers receiving $5,000 or more

Whether they received:

Direct compensation

Indirect compensation

Whether required disclosures were provided

This is where fiduciaries often admit conflicts.

III. Example: Principal and SageView Both Admit Indirect Compensation

A. Principal Life Insurance Company (Recordkeeper)

On Schedule C, page 2, the plan lists Principal Life Insurance Company as a service provider:

Role: Contract Administrator / Recordkeeper

Direct compensation: $158,327

Indirect compensation: “Yes” (explicitly checked)

Principal is identified as a party in interest

LakeshoreSelect24

This matters because:

A recordkeeper receiving indirect compensation is, by definition, receiving payments from sources other than the plan sponsor

Those payments often come from:

Proprietary investment products

Revenue sharing

Insurance spread profits

When the recordkeeper is also offering proprietary investments, ERISA §406(b) is immediately implicated

B. SageView Advisory Group, LLC (Investment Advisor)

The same Schedule C shows:

SageView Advisory Group, LLC

Role: Investment Advisory

Direct compensation: $59,924

Indirect compensation: “Yes”

Amount of indirect compensation reported: $16,898

LakeshoreSelect24

This is a critical red flag:

An investment advisor receiving indirect compensation is no longer acting solely on behalf of the plan.

This opens the door to:

ERISA §406(b)(1): acting for one’s own account

ERISA §406(b)(3): receipt of consideration from third parties

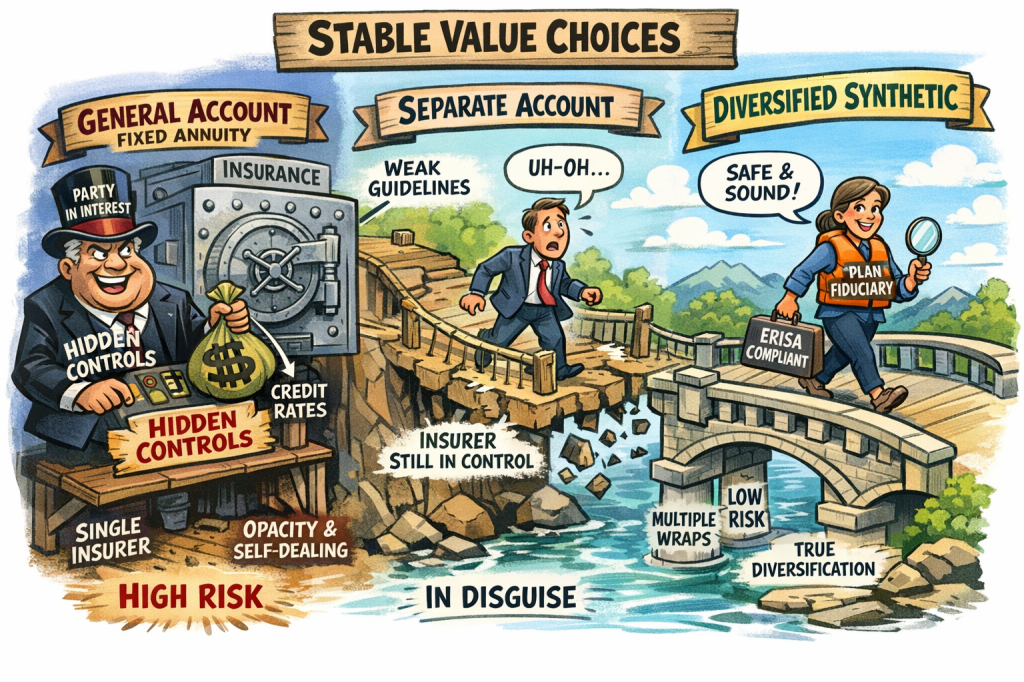

For more than 30 years, “stable value” has been marketed to retirement plan fiduciaries as a conservative, low-risk, bond-like option. That description is only accurate for one form of stable value: diversified synthetic stable value.

General Account (GA) and Separate Account (SA) stable value products are fundamentally different. They embed insurance spread products, opaque crediting decisions, and conflicted compensation structures that directly collide with ERISA’s duties of loyalty, prudence, and prohibited-transaction rules.

This distinction is not academic. It is measurable, documented, and long recognized in the academic literature.

I. The Academic Baseline: General Account Risk Is an Order of Magnitude Higher

In The Handbook of Stable Value Investments (Frank J. Fabozzi, ed., 1998), Jacqueline Griffin’s chapter on wrap provider credit risk demonstrates that general account stable value products carry roughly ten times the credit risk of diversified synthetic GIC structures. https://www.amazon.com/Handbook-Stable-Value-Investments/dp/1883249422

Why?

Because in a general account product:

Participants are exposed to the entire insurer balance sheet

Assets are commingled with unrelated insurance liabilities

Returns are driven by insurer spread management, not portfolio performance

Risk is single-entity, undiversified credit risk

Synthetic structures, by contrast, isolate risk, diversify exposure, and enforce constraints.

This is not a matter of opinion. It is structural.

II. What Makes Synthetic Stable Value Fundamentally Different

Diversified synthetic stable value is not an insurance product. It is a bond portfolio plus third-party guarantees.

Its defining features are:

1. Enforced investment guidelines

Duration limits

Credit quality floors

Sector concentration caps

Prohibited asset classes

These guidelines are contractual and enforceable, not aspirational.

2. Independent wrap providers

Multiple, unrelated wrap issuers

Diversified counterparty exposure

No dependence on a single insurer’s solvency

3. Transparent crediting-rate formulas

Crediting rates are formula-driven

Inputs are observable: yield, duration, market-to-book ratio

No discretionary “pricing committee” authority

4. No embedded spread product

No insurer decides how much return to “pass through”

No opaque profit margin extracted from participant balances

This structure aligns cleanly with ERISA fiduciary principles:

Diversification

Transparency

Process discipline

Arm’s-length pricing

That is why synthetic stable value does not raise inherent prohibited-transaction concerns.

III. General Account Stable Value: A Prohibited Transaction by Design

General Account stable value products invert every one of those principles.

A. Single-entity credit risk

A GA stable value fund is simply a fixed annuity backed by the insurer’s general account. Participants bear:

From an ERISA perspective, SA products remain conflicted insurance arrangements, not arm’s-length investment products.

V. The Efficient Frontier Confirms the Legal Analysis

Your Stable Value Efficient Frontier work shows what theory predicts:

Synthetic stable value delivers higher risk-adjusted returns

GA and SA products underperform after adjusting for credit risk

The “stability” premium is purchased with hidden tail risk

In other words, GA and SA products are not just legally problematic — they are economically inferior.

That makes their selection even harder to defend under ERISA’s prudence standard.

VI. Why This Matters for Litigation and Fiduciary Oversight

The takeaway is simple:

Synthetic stable value

Diversified

Transparent

Formula-driven

Consistent with ERISA duties

General Account stable value

Single-entity credit risk

Discretionary insurer pricing

Embedded self-dealing

Inherently conflicted

Separate Account stable value

Cosmetic separation

Weak constraints

Same economic conflicts

Courts have increasingly recognized that process matters. When fiduciaries choose GA or SA products over available synthetic alternatives, they are not just choosing a different implementation — they are choosing a conflicted structure.

That is why GA and SA stable value products should be analyzed not merely as “imprudent,” but as ERISA prohibited transactions.

VII. Conclusion: Stable Value Done Right — and Done Wrong

Stable value itself is not the problem.

Insurance-based stable value is the problem.

Diversified synthetic stable value shows that it is entirely possible to deliver capital preservation, liquidity, and reasonable returns without exposing participants to insurer balance-sheet risk or conflicted rate-setting.

When fiduciaries instead choose GA or SA products, they are choosing opacity, concentration, and conflicted compensation — the very conditions ERISA was designed to prevent.

—————————————-

Why General Account (GA) and Separate Account (SA) Are ERISA Prohibited Transactions — and Diversified Synthetic Is Not

Feature

General Account (GA) Stable Value

Separate Account (SA) Stable Value

Diversified Synthetic Stable Value

Underlying structure

Fixed annuity backed by insurer’s entire general account

Insurer-managed separate account marketed as “bond-like”

Diversified bond portfolio + third-party wrap contracts

Primary risk bearer

Plan participants (single insurer credit risk)

Plan participants (still insurer-controlled)

Participants bear diversified bond risk; wrap providers guarantee liquidity

Explicit spread product (insurer profits from rate suppression)

Spread product remains

No embedded spread

Liquidity / exit risk

Contract-value limits; MVAs possible

Similar termination risk

Liquidity guaranteed by wraps, subject to formula

Diversification

None (single insurer)

Limited / illusory

True diversification

Party-in-interest status

Insurer is a party in interest

Insurer is a party in interest

Wrap providers are arms-length counterparties

ERISA §406(b) self-dealing risk

High – insurer sets returns for its own account

High – insurer controls rate setting

Low – no discretionary self-pricing

ERISA §404 prudence alignment

Weak (opaque, concentrated risk)

Weak (misleading structure)

Strong (process-driven, diversified)

Regulatory oversight

State insurance regulators

State insurance regulators

Plan fiduciaries + contractual oversight

Typical marketing narrative

“Guaranteed,” “safe,” “principal protected”

“Synthetic-like,” “separate,” “safer GA”

“Institutional,” “transparent,” “bond-based”

Economic reality

Insurance balance-sheet exposure

Insurance balance-sheet exposure with cosmetic separation

Bond portfolio + diversified liquidity protection

ERISA litigation posture

Inherently conflicted; prohibited transaction

Conflicted; prohibited transaction

Defensible investment structure

General Account and Separate Account stable value products embed insurer self-dealing, discretionary pricing, and single-entity credit risk, making them structurally incompatible with ERISA’s duties of loyalty and prohibited-transaction rules — while diversified synthetic stable value does not.

Journal of Economic Issues Thomas E. Lambert University of Louisville, Christopher B. Tobe , ““Safe” Annuity Retirement Products and a Possible U.S. Retirement Crisis,” https://ir.library.louisville.edu/faculty/943/

In late 2025, independent journalist and teacher Jim Vail documented a striking confrontation between Teacher Trustee Erika Meza and the Chicago Teachers’ Pension Fund’s external consultant, Callan Associates, at a board meeting on December 11, 2025. The exchange highlights the growing tension between rank-and-file educator fiduciaries and institutional insiders pushing private markets — especially private equity — with all of the attendant cost, complexity, and opacity that has plagued many U.S. public pension systems. secondcityteachers.substack.com

A. Callan’s Defense of Private Equity Met With Skepticism

At the board meeting, Callan consultant Angel Haddad presented an upbeat defense of private equity, emphasizing “diversification” outside of traditional public equities and claiming that private equity offers exposure to businesses that might not otherwise be accessible. Haddad argued that private equity can provide “different return sources” for the pension fund. secondcityteachers.substack.com

Trustee Meza pushed back forcefully on several fronts:

She highlighted the cost structure of private equity, including fees and carried interest, questioning whether the net returns justified the risk and cost. secondcityteachers.substack.com

She pointed out that CTPF has a large number of managers relative to other large plans, and that the plan conducts frequent RFPs — “unheard of” in size and frequency, suggesting manager proliferation and consultant facilitation without demonstrable benefit.secondcityteachers.substack.com

She directly asked Callan to prepare a true opportunity-cost comparison between the private equity portfolio and simple public market benchmarks (e.g., Russell 3000), including all fees and projected distributions. secondcityteachers.substack.com

She questioned the fee structure for private equity manager searches, pointing out that CTPF paid Callan roughly $25,000 per search, an amount nearly equal to the cost of a three-day board trip. secondcityteachers.substack.com

Meza also observed (echoing academic research) that there is “mounting evidence that private equity is not outperforming a regular index fund” net of fees, and that the risk–return profile (higher volatility for marginal return improvement) may be unfavorable. secondcityteachers.substack.com

B. The Broader Context: Consultant Conflicts of Interest

This boardroom clash is not an isolated event — it reflects a systemic issue within the institutional consulting industry.

An analytical piece circulated in late 2025 argues that the largest pension consultants — including firms like Mercer, Aon, Russell, Wilshire, and even “independent” firms such as Callan — have become the distribution arm for private equity and private credit.The CommonSense 401k Project

Key points from this industry analysis include:

Many major consultants are now owned by private equity firms, publicly traded with shareholder incentives to grow high-fee areas, or structured so that consultant compensation increases materially when clients allocate more to private markets. The CommonSense 401k Project

Even independent, employee-owned consultants like Callan are implicated because they:

charge premium fees for alternative consulting services;

operate “paid access” events such as Callan College, where private markets managers pay for exposure to pension clients (a “pay-to-play” dynamic); and

have internal compensation structures that reward consultants for growing alternative allocations. The CommonSense 401k Project

This creates an economic incentive tied not to net performance for beneficiaries, but to the expansion of high-fee private investments. The CommonSense 401k Project

In short, when consultants benefit structurally from helping private equity and credit grow within pension portfolios, their advice can no longer be presumed neutral or purely fiduciary — it is shaped by economic incentives that may be anti-beneficiary.

C. Confirmation from Chicago Trustee Questions

Across multiple meetings, Chicago Teachers trustees — both active and retired — have begun to question the role and performance of private markets allocations:

Another trustee asked why Callan was not present or vocal in the decision process for new private equity commitments, despite being paid to vet these investments. secondcityteachers.substack.com

Trustees also flagged questionable travel and due-diligence practices (e.g., a CIO trip to South Africa with unclear justification), underscoring weak internal oversight and consultant dependency. secondcityteachers.substack.com

At least some trustees pushed back on relying solely on external narratives without transparent risk/return comparisons to public markets. secondcityteachers.substack.com

D. Public Pension Underfunding and Risk

The backdrop to these governance tensions is sobering: Chicago’s pension funds are among the most underfunded in U.S. history, with Chicago Police and Teachers plans facing deep fiscal stress attributable in part to high-cost, opaque alternative allocations and compounding actuarial pressures (a theme explored elsewhere in my Chicago Police Pension work). Wirepoints

Private equity — attractive in theory — is increasingly questioned by trustees who see:

performance shortfalls,

high fee drag,

limited liquidity,

and opaque valuations.

Despite these realities, consultants continue to advocate for expanded private markets commitments, creating friction between fiduciary responsibility and consultant incentives.

E. Hypocrisy of Charter-Aligned Investment Narratives

A further dimension of consultant capture relates to alignment of values and investment narratives. For example, some consultants and practitioners argue that private equity can finance projects like affordable housing or economic development, enabling social goals. secondcityteachers.substack.com

Yet this often sits alongside:

Investments in charter school facilities or charter-aligned companies (which raise political/ideological concerns for many public educators),

A lack of member disclosure about how fees and management decisions support private markets interests,

And, as seen in other contexts (e.g., CalPERS, Kentucky Teachers), fiduciary narratives that prioritize consultant comfort over member outcomes.

Chicago trustees like Meza have pointed directly to the need for clarity on fees, opportunity costs, and benchmark comparisons, and against simply repeating diversification rationales that assume complexity is a virtue. secondcityteachers.substack.com

F. Takeaway: Governance, Fiduciary Duty, and Pension Reform

Jim Vail’s coverage — and the trustees’ questioning — highlights several key governance challenges now emerging across teacher pension funds:

Consultant incentives often diverge from beneficiary best interests, particularly around private markets expansion. The CommonSense 401k Project

Opaque valuations, smoothed return profiles, and non-investable benchmarks require trustees to demand better risk/return transparency. The CommonSense 401k Project

Trustees with fiduciary courage (like Erika Meza) are pushing back on narratives that protect consultant interests rather than member outcomes. secondcityteachers.substack.com

Public pension underfunding and elevated risk mean that expanded private markets exposure warrants heightened scrutiny, not automatic endorsement. Wirepoints

Hypocrisy and conflict concerns (e.g., charter connections and political influence) underscore the need for clear disclosure and accountability.

Redactions are often justified as protecting “trade secrets,” “privacy,” or “ongoing investigations.” In practice, across public pensions, private-equity contracts, and the Epstein files, redactions serve a different function: concealing power, conflicts, leverage, and legal exposure.

The same institutional logic governs all three domains:

Redactions are not about secrecy for safety — they are about secrecy for control.

Public pension systems like CalPERS, OPERS, and Kentucky Retirement Systems, private-equity limited partnership agreements, and the Epstein financial files all exhibit the same pattern:

Lawful access exists

Disclosure is nominally promised

Key economic and governance provisions are systematically hidden

The hidden provisions implicate fiduciary breaches, political influence, or criminal exposure

This is not accidental. It reflects a shared ecosystem of elite finance, legal privilege, and political insulation.

I. Redactions in Public Pensions: Not Trade Secrets, but Fiduciary Violations

Public pension plans are governed by fiduciary law, not private-contract law. Their records are presumptively public. Yet, over the last 10–15 years, pension systems increasingly adopted private-equity redaction norms that contradict their statutory obligations.

What is Redacted — and Why It Matters

Your Essex Woodlands comparison (Kentucky unredacted vs. Ohio redacted) shows that redactions systematically hide:

Hidden leverage

110% investment authority

Subscription-based leverage

Short-term borrowing authority

Excessive and opaque fees

Management fees disguised as quarterly percentages

Organizational expense caps vastly exceeding actual costs

Special GP distributions and expense reimbursements

Fiduciary breaches embedded in contract design

Heads-I-win / tails-you-lose allocation of risk

GP discretion over valuation, timing, and distributions

Weak or illusory clawbacks

Offshore custody and jurisdictional opacity

Non-US domiciles

Offshore SPVs and holding structures

Advisory committee composition

Names redacted because they reveal conflicts, inducements, or political access

These are not trade secrets. They are terms governing public money, and in many states they likely violate fiduciary statutes outright.

Your Ohio and Kentucky statutory analysis is crucial:

Many state fiduciary codes do not even list limited partnerships as permissible investments

Custody, diversification, leverage, and prudence standards are incompatible with these hidden provisions

Redaction is the mechanism that allows illegal investments to persist without challenge.

II. The Normalization of Redaction Through Private Equity

Private equity did not just benefit from redactions — it institutionalized them.

Historically:

Public pensions required RFPs, competitive bidding, and disclosures

Contracts were subject to open-records laws

Political donations were capped and disclosed

Post-Citizens United:

PE firms lobbied for RFP carve-outs

“Trade secret” exemptions were expanded

Limited partnership agreements became the de facto governing documents

Consultants and lawyers normalized redaction as “industry standard”

What changed was not the law — it was enforcement culture.

The result:

Secret, no-bid contracts

Benchmark engineering

Consultant-blessed opacity

Pay-to-play without receipts

Redactions are the operating system of this regime.

III. Epstein Files: The Same Redaction Logic, Different Crime

The Epstein files expose the same structural pathology at a higher criminal level.

What Was Redacted — and Why

In Epstein-related disclosures:

Names of financiers, lawyers, trustees, and intermediaries were withheld

Banking relationships were obscured

Offshore structures were shielded

Correspondence revealing knowledge (not just participation) was suppressed

The justification again was:

Privacy

Ongoing investigations

Risk of defamation

But as your Epstein article correctly notes, the files reveal:

“Not just pedophiles — but a corrupt offshore financial system.”

The redactions protected:

Enablers, not victims

Institutions, not individuals

Networks, not isolated actors

Just as in public pensions, redaction functioned as a liability firewall.

IV. The Common Denominator: Elite Financial Immunity

Across all three domains — pensions, private equity, Epstein — the same actors recur:

Global law firms

Private banks

Offshore administrators

Consultants and “independent” advisors

Politically connected intermediaries

The same techniques recur:

Jurisdictional fragmentation

Complexity as camouflage

Delegation to “experts”

Legal privilege as a shield

Redaction as a substitute for accountability

This is why redactions escalate when:

Performance deteriorates

Scrutiny increases

Political stakes rise

Opacity is not incidental — it is defensive architecture.

V. Why This Matters Now: CalPERS and the Next Phase

CalPERS sits at the center of this ecosystem:

One of the world’s largest private-equity investors

A key political actor in California

A template for other pension systems

A beneficiary of consultant-engineered benchmarks and compensation schemes

The same redaction logic now extends to:

Executive compensation justification

Performance benchmarking

Liquidity risk disclosures

Political relationships

Contractual fee structures

As you’ve documented repeatedly, redactions are the glue that holds the system together.

VI. Conclusion: Redactions Are the Scandal

The scandal is not just:

Private equity underperformance

Excessive fees

Epstein’s crimes

Pension mismanagement

The scandal is the shared refusal to disclose.

Redactions transform:

Fiduciary violations into “complexity”

Conflicts of interest into “customary practice”

Political influence into “coincidence”

Criminal facilitation into “privacy concerns”

Until redactions are treated as prima facie evidence of risk and misconduct, public institutions will continue to hemorrhage money, trust, and legitimacy.

Sunlight is not a threat to honest systems. Redactions are a confession by dishonest ones.

Introduction — Beyond Disclosure, Into violating ERISA Fiduciary Law

This Appendix analyzes how the embedding of lifetime income annuity elements inside Target-Date Funds (TDFs) violates core provisions of the Employee Retirement Income Security Act (ERISA). It updates the analysis laid out in:

By examining the structure of modern TDFs — particularly those using state-regulated CITs and insurance-wrapped annuity components — this Appendix explains why such constructions are not merely risky or opaque, but in many cases incompatible with ERISA’s fiduciary duties of prudence, loyalty, and prohibited-transaction regime.

2. Lifetime Income “Guarantees” Inside TDFs: Substance Over Form

Target-Date Funds increasingly include lifetime income features — either through internal sub-portfolios or embedded insurance wrappers — promising participants “guaranteed income for life.” But these guarantees are not financial alchemy; they derive from general-account fixed annuities and similar insurance obligations that:

Are backed by the balance sheet of a single insurer;

Are priced using internal actuarial assumptions, not market pricing;

Depend on insurer discretion over crediting rates and contractual terms;

Obscure spread-based profits and other indirect compensation.

As explained in Annuities Are a Prohibited Transaction, these characteristics are not neutral features — they are economic modalities that define an insurance contract, not a diversified investment. Embedding them inside TDFs does not change their legal character; it simply hides them behind the Target-Date label.

3. ERISA §404 — Breaches of Prudence and Loyalty

ERISA §404(a)(1)(B) and (C) require fiduciaries to act with the care, skill, prudence, and diligence of a prudent expert and to diversify plan investments to minimize the risk of large losses.

A. Imprudent Integration of Insurance Risk

Lifetime income annuity elements impose single-entity credit risk on participants because the guarantees depend entirely on the solvency and internal pricing of one insurer’s general account. As has been documented in the TDF corruption analysis, investors often do not even realize they hold such exposures because:

TDFs use state-regulated CIT structures that mask the insurance component,

Consultants and recordkeepers classify these as “stable income” or “income enhancement.”

But from an economic perspective, a TDF containing a general-account annuity is functionally similar to a 401(k) that has placed a portion of participant assets into a fixed annuity inside an insurance general account — a structure courts have found problematic and ERISA fiduciaries must evaluate rigorously.

B. Improper Diversification

Diversification requires more than a target asset mix; it demands avoidance of undiversified exposures that can materially threaten principal. Embedding a single insurer’s guarantee into a diversified TDF portfolio does not diversify the insurer credit risk; it adds an undiversified risk factor.

The duty of loyalty is similarly breached when fiduciaries accept such exposures without transparent analysis and without evidence that the supposed lifetime income benefits outweigh the concentrated risk and fee opacity.

4. ERISA §406 — Hidden Prohibited Transactions

ERISA §406(a) prohibits plan assets from being used in transactions involving a party in interest, including insurers and service providers, unless an exemption applies.

A. The Per Se Nature of Annuity Transactions

Lifetime income guarantees embedded in TDFs are derived from contractual relationships with insurers or their affiliates — parties in interest. Even if indirectly accessed through a CIT, the economic reality is that:

Plan assets are committed to support insurance liabilities;

Insurers extract spread income and embedded profits;

Affiliated service providers benefit financially.

This meets the definition of a §§406(a) prohibited transaction: the plan transfers value to a party in interest, often in the form of fees and spread retention, without contemporaneous best-interest justification.

B. Failure of Prohibited-Transaction Exemptions

As detailed in Annuities Are a Prohibited Transaction, typical regulatory exemptions (e.g., PTE 84-24, PTE 2020-02) often cannot apply because lifetime income products:

Fail to disclose all compensation clearly;

Lack meaningful downgrade or termination provisions;

Do not center participants’ best interests;

Are structured with conflicts (e.g., insurer also acting as recordkeeper).

Thus, even if promoters claim exemption compliance, the underlying economics do not satisfy the statutory criteria.

5. Citations from the TDF Corruption WSJ Analysis: Valuation and Transparency Risk

The Wall Street Journal story When Your Private Fund Turns $1 Into 60 Cents underscores a related structural issue: valuation opacity. When private assets once thought to be “stable” were exposed to market pricing, they collapsed in value. This same dynamic exists, often unobserved, in TDFs that:

Hold non-transparent, non–market-priced private assets;

Embed insurance guarantees with discretionary valuations;

Report net asset values that are not subject to real-time market verification.

State-regulated CITs serve as the vehicle that allows this opacity to be recorded on participant statements as if it were transparent, diversified investment exposure. This practice is inconsistent with ERISA fiduciary norms requiring accurate valuation and disclosure.

6. ERISA’s Prohibition on Conflicted Compensation

ERISA §408(b)(2) demands that compensation be reasonable and disclosed. Lifetime income guarantees inside TDFs obscure significant compensation:

Insurance spreads not captured in traditional fee tables;

Embedded guarantee costs not disclosed as numeric fees;

Ancillary revenues to affiliates (e.g., asset-management fees, revenue sharing).

This is precisely the kind of undisclosed economic benefit that ERISA’s prohibited transaction and fiduciary standards were designed to prevent.

8. Participant Harm — The Ultimate Consequence

Lifetime income elements inside TDFs:

Increase cost without commensurate benefit;

Conceal risk behind “guarantee” language;

Reduce liquidity and choice;

Mask fees through the attribution of spread income;

Potentially deliver lower lifetime wealth than diversified non-annuitized options.

This harm is not speculative; it is structural.

9. Conclusion: Structural Incompatibility with ERISA

Lifetime income annuity components hidden within Target-Date Funds — particularly in state-regulated CIT structures — are not merely risky investment choices. They are:

Prohibited transactions with parties in interest under ERISA §406(a);

Inconsistent with required fiduciary processes, including valuation, disclosure, and conflict management.

Policymakers, litigators, and fiduciaries alike must recognize that the packaging of insurance guarantees inside TDFs does not transform them into safe, diversified investment exposures. It transforms them into trust law liabilities waiting to be litigated.

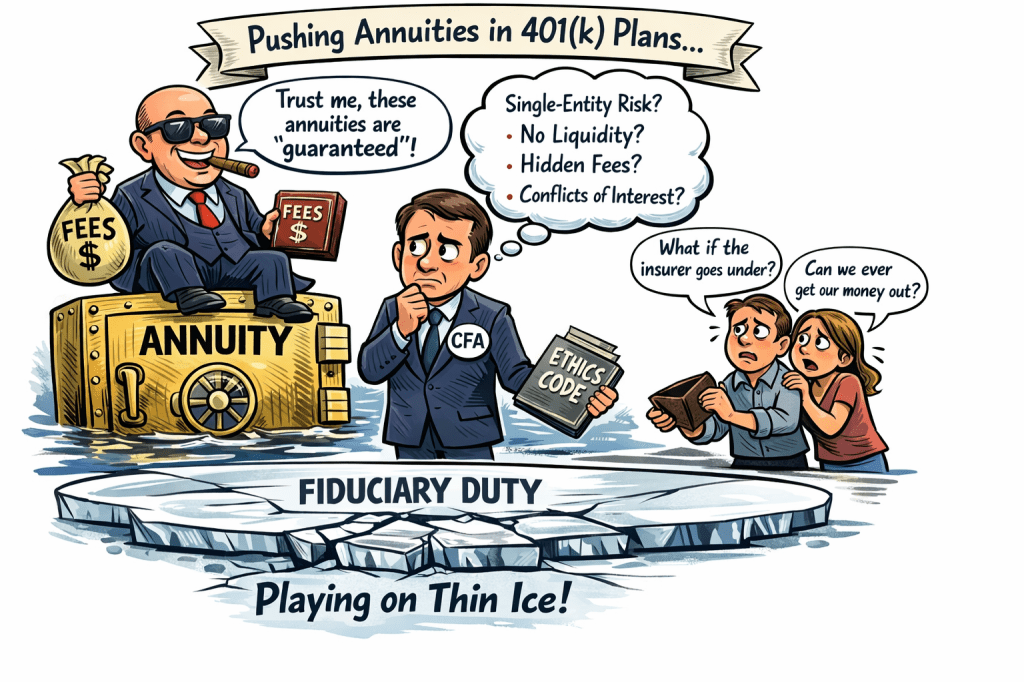

I.APPENDIX Introduction: Annuities as a CFA Ethics Issue, Not Merely an ERISA Issue

A few CFA charterholders has begun actively promoting lifetime annuities in 401(k) plans, often framing these products as prudent solutions to longevity risk. As discussed in 401(k) Lifetime Income: A Fiduciary Minefield (Commonsense 401k Project, Feb. 10, 2022), this framing ignores fundamental fiduciary risks embedded in annuity products—particularly single-entity credit risk, illiquidity, opaque pricing, and conflicts of interest.

While ERISA fiduciary standards already raise serious concerns, CFA Institute fiduciary and ethical standards are at least as strict—and in several respects stronger. CFA charterholders are bound not only by applicable law (including ERISA), but by an independent professional code that places client interests, transparency, and integrity of the profession above product sales or industry narratives.

This appendix demonstrates that actively recommending annuities in 401(k) plans may run afoul of multiple CFA Institute standards, particularly where the risks and conflicts inherent in annuities are minimized, obscured, or ignored.

II. CFA Institute Pension Trustee Code: Knowledge, Liquidity, and Prudence

The CFA Institute Pension Trustee Code of Conduct makes explicit that effective fiduciaries must understand:

“How investments and securities are traded, their liquidity.” (CFA Institute Pension Trustee Code of Conduct, p. 13)

This requirement is critical for annuities.

A. Liquidity Failures of Annuities

Lifetime annuities in 401(k) plans typically:

Cannot be traded,

Cannot be priced daily by a market,

Cannot be exited without penalty,

Are subject to insurer-controlled crediting rates and withdrawal restrictions.

A CFA charterholder who recommends a product whose liquidity disappears precisely when credit risk rises is failing the Code’s requirement of competence and diligence. Liquidity risk is not ancillary—it is central to DC plan design, where participants may need to rebalance, roll over, or withdraw assets.

III. Core Fiduciary Obligations Under the CFA Pension Trustee Code

The Pension Trustee Code requires fiduciaries to:

Act in good faith and in the best interests of participants

Act with prudence and reasonable care

Act with skill, competence, and diligence

Maintain independence and objectivity

Avoid conflicts of interest

Communicate transparently and accurately

Each of these principles is strained—if not violated—by annuity recommendations.

A. Prudence and Diversification

Diversification is a foundational fiduciary principle. Annuities concentrate participant assets in a single insurer, creating uncompensated single-entity credit risk. This violates both ERISA §404(a)(1)(C) and CFA prudence standards.

CFA charterholders routinely criticize concentrated credit exposure in bond portfolios—yet often ignore the same risk when it is embedded in an insurance product.

B. Transparency and Communication

Annuities:

Do not disclose spread-based compensation in a form comparable to expense ratios,

Do not disclose CDS-implied credit risk,

Do not provide transparency into offshore reinsurance or private credit backing liabilities.

Recommending such products without full transparency conflicts directly with the obligation to communicate accurately and transparently with beneficiaries.

IV. “Putting Clients First”: The CFA Code of Ethics

Every CFA charterholder annually affirms adherence to the CFA Code of Ethics and Standards of Professional Conduct, including the obligation to:

“Place the integrity of the investment profession and the interests of clients above their own personal interests.”

This is the essence of fiduciary duty.

A. Annuities and Asymmetric Incentives

Annuities generate profits through:

Spread income,

Illiquidity,

Opacity,

Long-dated lock-in.

These features benefit insurers and intermediaries—not participants. When CFA charterholders promote annuities while downplaying these structural incentives, they elevate product narratives over client welfare.

V. Application of CFA Standards to Annuities

Standard III(A): Loyalty, Prudence, and Care

Insurers exploit information asymmetry, :

Complexity,

Illiquidity,

Participant unfamiliarity with insurance accounting.

Recommending such products without full disclosure fails the duty to act for the benefit of clients.

Standard III(B): Fair Dealing

In annuities, insurers reserve discretion over:

Crediting rates,

Portfolio allocation,

Reinsurance structures.

Participants bear downside risk, while insurers retain upside discretion—mirroring the “GP discretion” clauses widely criticized in PE LPAs.

Standard III(D): Performance Presentation

Annuity performance is often:

Presented using smoothed or declared rates,

Not benchmarked to appropriate alternatives,

Compared misleadingly to money market funds rather than diversified stable value funds.

This selective presentation is inconsistent with fair and complete performance communication.

Standard VI(A): Conflicts of Interest

Conflicts arise where:

Insurers also serve as recordkeepers,

Consultants have relationships with insurers,

Products generate hidden spread income.

Failure to disclose or mitigate these conflicts violates CFA conflict-of-interest standards.

Standard VI(B): Priority of Transactions

Annuities prioritize insurer balance-sheet management over participant flexibility—similar to PE structures that prioritize GP economics over LP outcomes.

Standard VI(C): Fee Disclosure

Just as PE firms have been sanctioned for undisclosed fees, annuity providers:

Fail to disclose spread income,

Embed costs in opaque crediting rates,

Avoid standardized fee reporting.

CFA charterholders who accept this opacity are applying a double standard.

Standard VII(A): Conduct as a CFA Charterholder

By recommending products that violate principles of:

Transparency,

Diversification,

Liquidity,

Conflict avoidance,

CFA charterholders risk cheapening the CFA designation itself

VI. “50 Ways to Restore Trust in the Investment Industry”—Applied to Annuities

The CFA Institute’s 50 Ways to Restore Trust emphasizes:

Naming unethical behavior,

Advocating for stronger investor protections,

Refusing willful ignorance,

Holding bad actors accountable.

Silence around annuity risks—particularly by CFA charterholders—runs counter to this mandate. Ignoring annuity conflicts because they are “legal” or “industry standard” is precisely the ethical failure the CFA Institute has warned against.

VII. Conclusion: Annuities as an Ethical Stress Test for the CFA Profession

Pushing annuities into 401(k) plans is not merely a product choice—it is an ethical stress test for fiduciaries and CFA charterholders.

Annuities violate diversification principles.

They suppress risk-mitigation tools like downgrade provisions and CDS analysis.

They depend on opacity and illiquidity for profitability.

They expose participants to risks they cannot manage or exit.

Under CFA standards—particularly the Pension Trustee Code and the Code of Ethics—putting clients first requires resisting products whose economics depend on clients not fully understanding the risks.

If CFA charterholders apply to annuities the same ethical scrutiny they apply to other assets, many annuity recommendations in 401(k) plans would be indefensible.

Private credit has become the darling asset class of pensions, endowments, insurers, and increasingly retail investors. It promises what every fiduciary wants to hear: near-equity returns, bond-like stability, and low correlation to markets. But as scrutiny increases—from PBS NewsHour, Bloomberg, academics, and regulators—the uncomfortable question is no longer whether private credit is risky.

It is whether the performance itself is real.

Start With the Basic Economic Reality of Credit Markets

Credit markets are among the most competitive markets in finance.

In real-world lending:

10 basis points (0.10%) matters.

Borrowers arbitrage relentlessly between banks, public bonds, syndicated loans, and revolvers.

If a borrower can save 25–50 bps, they usually do.

This means true economic excess returns in credit are small unless you are:

taking materially more risk,

exploiting a temporary dislocation, or

benefiting from non-price advantages that are not scalable.

There is no magic fourth option.

Now Add Private Credit Fees — This Is Where the Story Breaks

Private credit typically charges, conservatively:

~100 bps management fee,

10–20% performance fee (“carry”),

plus fund expenses, leverage costs, and transaction fees.

Let’s translate that into economics.

Example (simplified but realistic):

Gross loan yield: SOFR + 450 bps

SOFR: 5.0%

Gross yield: 9.5%

Subtract:

Management fee: –1.0%

Fund expenses & financing drag: –0.3%

Expected carry (annualized): –0.7%

➡️ Net to LP ≈ 7.5%

Now ask the obvious question:

If the same borrower can access public credit or bank credit at SOFR + 250–300 bps, why is private credit earning SOFR + 450?

Answer: It usually isn’t—not without additional risk or accounting distortion.

Jeffrey Hooke and the “Mark-to-Myth” Problem

This is where the recent research by Jeffrey Hooke (Johns Hopkins), Xiaohua Hu, and Michael Imerman becomes pivotal.

In their Journal of Private Markets Investing article, the authors do something refreshingly simple: They compare private credit funds to publicly traded ETFs with similar underlying assets, instead of the industry’s preferred, forgiving benchmarks.

Their findings are devastating:

Private credit funds barely outperform or underperform comparable public benchmarks.

Much of the reported “performance” comes from unrealized residual value—loans that have not been repaid and are not marked to market.

This is “mark-to-myth” accounting, eerily similar to illiquid public investments before the Global Financial Crisis

Why Private Credit is a Fraud

.

As Hooke put it bluntly:

“Private credit performance is both lacking in alpha as well as a timely return of capital. The two main marketing points of the industry seem to be illusory.”

Why Private Credit is a Fraud

That is not activist rhetoric. That is an academic indictment.

The Five Ways Private Credit ‘Works’ — None Are Free

There are only five possible explanations for private credit’s reported success:

1. Illiquidity Premium (Overstated)

True illiquidity premia in credit are typically 25–75 bps, not 200–300 bps. Yet private credit markets:

offer quarterly liquidity,

have active secondaries,

and show “smooth” NAVs.

That’s not illiquidity. That’s delayed price discovery.

2. Covenant and Structural Risk

Private credit often:

lends to weaker borrowers,

accepts looser covenants,

uses PIK toggles and amend-and-extend,

relies on sponsor goodwill rather than enforceable protections.

This isn’t alpha. It’s selling insurance against default and downgrade.

3. Regulatory Arbitrage

Private credit fills gaps where:

banks are constrained by capital rules,

borrowers fail public-market disclosure tests.

That’s not superior underwriting. It’s regulatory arbitrage, and it disappears when losses arrive.

4. Valuation Smoothing (The Big One)

Private credit is not market-tested:

loans are marked by managers or friendly third parties,

downgrades are slow,

non-accrual is delayed,

restructurings avoid default recognition.

Result:

volatility is suppressed,

losses are deferred,

fees keep flowing.

Public credit shows pain early. Private credit hides it.

5. Survivorship and Selection Bias

What you see:

successful funds,

cherry-picked vintages,

IRRs boosted by cash-flow timing.

What you don’t:

funds quietly wound down,

capital impairment absorbed years later.

Why Consultants and Pensions Love This Illusion

As discussed in my recent post on how pension consultants became the distribution arm for private equity, the same conflicts apply to private credit. Smoothed returns:

understate standard deviation,

understate correlation,

inflate Sharpe ratios,

and mechanically justify over-allocation.

The CFA Institute has explicitly warned that illiquid assets often exhibit stale and artificially smoothed returns, and that analysts “need to unsmooth the returns to get a more accurate representation of risk and return.”

Yet consultants rarely do.

Why This Matters for Pensions and ERISA Fiduciaries

For large plans:

Public credit costs <5 bps

Private credit costs 100–200+ bps all-in

The excess return hurdle must overcome:

fees,

illiquidity,

valuation opacity,

tail risk.

That is an extraordinary burden of proof—especially when borrowing spreads differ by tens of basis points, not hundreds.

Under ERISA principles, performance based on misleading valuation, smoothed risk, or delayed loss recognition raises serious questions about:

prudence,

reasonableness of fees,

and prohibited transactions.

This is not a theoretical concern. It goes directly to whether reported performance is materially misleading.

So… Is Private Credit Performance a Fraud?

Fraud requires intent. That is for regulators and courts to decide.

But systematic overstatement of returns, systematic understatement of risk, and performance driven by unrealized, unmarked residual value meet a lower—and more relevant—standard:

They mislead fiduciaries and beneficiaries about the true economics of the investment.

In a competitive credit market where 10 basis points matters, private credit cannot deliver persistent excess returns after 100-plus basis-point fees unless risk is being hidden, delayed, or transferred through opaque valuation and weak structures.

There is no third option.

Chris Tobe, CFA, CAIA has written extensively on Private Credit and its use in Public Pensions, and Life Insurance Portfolios backing annuities. He was awarded the Private Debt Microcredential in 2023 by CAIA. In his role as the Chief Investment Officer at Hackett Robertson Tobe in 2017 he completed a fiduciary review of the $4billion Private Credit Portfolio of the $40 billion Maryland State Retirement System. His upcoming paper in the Journal of Economic issues looks at the Private Credit portfolios backing annuities.

According to multiple reporting outlets, different private credit lenders have marked the identical Medallia loan at materially different values as of late 2025:

An Apollo Global Management private credit fund valued the loan at ~77 cents on the dollar (indicative of distress pricing). Private Debt News+1

A KKR co-managed vehicle marked the same loan significantly higher, at ~91 cents on the dollar. Private Debt News

In some fills of the same exposure by Blackstone’s BDC, values were reported between these levels, further highlighting divergence across managers. Private Debt News

This 14-cent or greater valuation gap on the same underlying asset — held contemporaneously by different private credit lenders — is among the largest spreads observed in regulatory filings to date, and underscores several important points for fiduciaries and analysts:

• Private credit valuations are highly discretionary

Unlike publicly traded bonds that have observable market prices, private credit lenders often determine marks based on internal assumptions regarding recoveries, default probabilities, liquidity, and expected cash flows. These assumptions can vary significantly across managers, even for the same borrower and capital structure.

• Reported performance is directly tied to valuation assumptions

Because private credit returns — particularly for illiquid loans — depend on periodic marks rather than realized cash flows, differences in pricing assumptions immediately translate into differences in reported returns. In the Medallia example, a 14-point valuation delta between Apollo and KKR alone would materially change realized and unrealized return metrics, absent any difference in actual credit performance.

• The divergence grows precisely where risk rises

As commentators noted, valuation spreads tend to widen especially when a loan is stressed. In the Medallia case, Apollo’s more distressed mark and KKR’s higher valuation reflect differing expectations about recovery and credit quality, rather than a single objective credit outcome. Private Debt News

• This kind of mark dispersion is incompatible with reliable performance reporting

If managers can assign widely divergent fair values to the same asset without observable market trades — and those marks drive net asset values (NAVs), performance statistics, fee calculations, and allocation decisions — then reported private credit performance is inextricably tied to manager discretion and valuation policy, rather than hard economic results.

In other words: when valuation assumptions vary by 14 points or more on identical exposures, reported returns cease to reflect reliable economic reality and instead reflect marking policy.

Implications for My Overall Thesis

This Medallia valuation discrepancy sits precisely at the juncture of the major themes in my reporting:

PBS and academic warnings about opaque valuations and illiquid asset risk; Accredited Insight

Consultants’ reliance on smoothed private credit returns to justify over-allocation;

The fundamental issue you raise: that private credit performance may not be grounded in observable market economics, but in manager discretion.

With this example, we can now point to actual data from regulatory filings and market reporting showing that even on the same risk exposure, private credit marks — and therefore reported returns — are not consistent, objective, or verifiable across major alternative asset managers.

This stands as one of the most compelling empirical pieces of evidence supporting my argument that private credit performance, as currently reported and used in fiduciary models, may be fundamentally misleading.

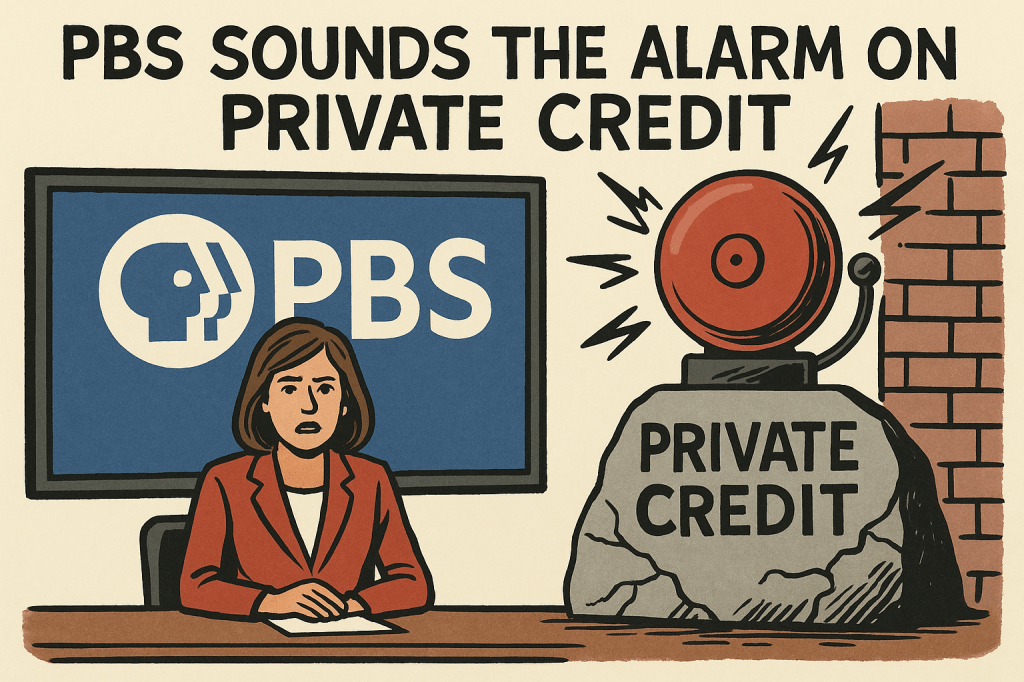

On December 11, 2025, PBS NewsHour did something that almost no mainstream media outlet has done to date: it warned the public—plainly and directly—about the risks of private credit. The segment, airing roughly between the 20- and 28-minute mark of the broadcast, treated private credit not as an exotic investment strategy for sophisticated institutions, but as a growing systemic risk that already touches ordinary Americans through pensions, insurance products, and retirement plans. https://www.pbs.org/video/december-11-2025-pbs-news-hour-full-episode-1765429201/

That alone is significant. PBS is not a sensationalist outlet. When PBS NewsHour devotes prime airtime to a financial product, it is usually because the issue has matured from “industry concern” into a matter of broad public interest and potential harm. Private credit has now crossed that threshold.

PBS Breaks the Silence on Private Credit Risk

What makes the PBS NewsHour segment so important is not just that it covered private credit, but how plainly it described the regulatory hole surrounding it. As PBS explained, “private credit is just lending by nonbanks — financial institutions like pension funds, insurance companies, sovereign wealth funds — but not regulated like the traditional banking system.” That simple framing strips away years of industry marketing and exposes the core issue: private credit performs a bank-like function without bank-level oversight.

Even more telling was the warning from Tom Gober, an insurance fraud examiner, who focused on who ultimately bears the risk. Gober stated: “A very large percent of the population is affected by this higher risk without knowing it.” That observation goes to the heart of the problem. Private credit risk is no longer confined to hedge funds or wealthy investors. It is increasingly embedded—quietly and indirectly—inside pension plans, insurance general accounts, pension risk transfer annuities, target date funds, and state-regulated collective investment trusts, where workers and retirees have no visibility, no pricing transparency, and no meaningful ability to opt out.

When PBS elevates this issue to a national audience, it confirms what fiduciary advocates have been warning for years: private credit is not just an alternative investment—it is a public exposure problem.

The BIS, Financial Times, and the Credit Ratings Problem

PBS’s warning aligns closely with concerns raised by global regulators. In a recent report highlighted by the Financial Times, the Bank for International Settlements (BIS) warned that private loan credit ratings may be “systematically inflated.” The BIS focused on the growing reliance on small or lightly regulated ratings firms—particularly in insurance and private credit markets—where inflated ratings can dramatically reduce capital requirements and mask real credit risk. https://www.ft.com/content/9d1f4e49-5edc-4815-9efb-d4ef41756d72

This is not an academic issue. Inflated ratings distort pricing, suppress risk premiums, and create the conditions for sudden repricing and fire sales when defaults rise or liquidity dries up. The BIS explicitly tied these dynamics to systemic fragility, drawing uncomfortable parallels to the mis-rated mortgage securities that fueled the 2008 financial crisis.

The danger is magnified because private credit assets are illiquid, thinly traded, and often self-priced. When confidence breaks, there is no transparent market to absorb losses—only forced write-downs that cascade through insurance balance sheets and pension portfolios.

What This Means for ERISA Plans and Retirement Savers

These systemic warnings directly reinforce the concerns raised earlier this year in my CommonSense 401k Project’s article, “Private Debt Problematic in ERISA Plans.” https://commonsense401kproject.com/2025/07/18/private-debt-problematic-in-erisa-plans/ As that piece explained, private debt and private credit are fundamentally misaligned with ERISA’s core fiduciary requirements of prudence, diversification, and fair valuation. This will be dealt with in litigation around prohibited transactions in which the burden of proof is on the fiduciary that their private debt is exempt.

Private credit’s lack of observable market pricing, combined with long lockups and opaque fee structures, makes it exceptionally difficult for plan fiduciaries to demonstrate that participants are receiving commensurate value for the risks being taken. Embedding these assets inside target date funds or insurance-wrapped vehicles does not solve the problem—it hides it.

PBS’s reporting underscores an uncomfortable truth: millions of retirement savers are already exposed to private credit risk without knowing it, precisely the scenario ERISA was designed to prevent.

Shadow Banking, Then and Now

None of this is new. Nearly a decade ago, analysts warned that private equity firms were evolving into shadow banks, providing credit outside the regulated banking system. That prediction has now fully materialized. Private equity sponsors control vast private credit platforms that originate, warehouse, and distribute loans with minimal public disclosure.

PBS’s segment confirms that these concerns are no longer fringe critiques—they are entering mainstream financial discourse.

Why the PBS Warning Matters Now

The convergence of warnings—from PBS, the BIS, the Financial Times, and independent analysts—signals that private credit has reached a dangerous inflection point:

It has grown to systemic scale

It operates largely outside traditional regulatory frameworks

Its risks are mispriced through inflated ratings

And its losses will not be confined to “sophisticated investors,” but absorbed by workers, retirees, and policyholders

When a trusted public broadcaster like PBS feels compelled to warn viewers, fiduciaries and regulators should take notice. The question is no longer whether private credit can create systemic problems—it is whether policymakers will act before those problems become visible through losses.

Conclusion: An Alarm Bell for Fiduciaries

PBS did not mince words, and neither should fiduciaries. Private credit is increasingly intertwined with retirement systems that were never designed to absorb opaque, illiquid credit risk. The warning from Tom Gober—that a large portion of the population is already exposed without knowing it—should be taken as a direct challenge to ERISA fiduciaries, regulators, and courts.

Transparency, prudence, and accountability are not optional under ERISA. If private credit cannot meet those standards, it does not belong in retirement plans—no matter how attractive the yield looks on paper.

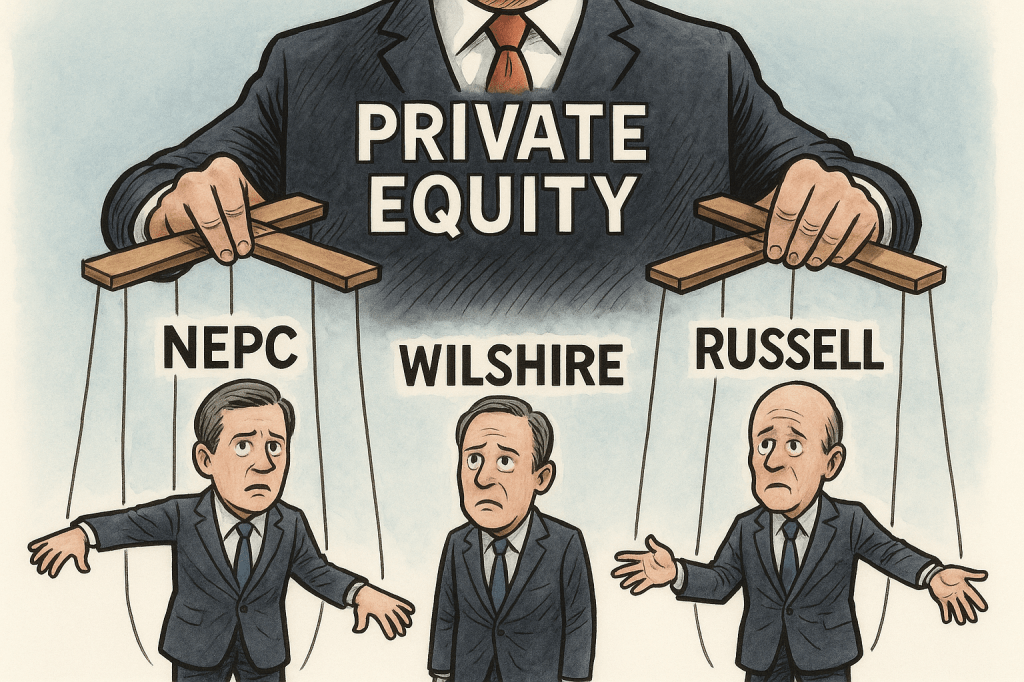

Employee-owned, publicly traded, or PE-backed—every major consultant now has financial incentives to push higher-fee private equity and private credit.

For years, institutional investment consultants have marketed themselves as independent fiduciaries guiding pension funds, 401(k) plans, endowments, and public retirement systems through the complexities of modern markets.

But the truth is far different. In 2025, the consulting industry has quietly transformed into the single most important distribution channel for private equity.

This shift cuts across every ownership model:

PE-owned consultants like NEPC (via Hightower/THL), Wilshire (CC Capital & Motive Partners), Russell Investments (TA Associates & Reverence Capital), and SageView (Aquiline).

Public-company-owned consultants like Mercer (Marsh & McLennan), Aon, and WTW—with earnings models tied to alternatives growth.

Employee-owned consultants like Callan, Meketa, RVK, Verus, and Marquette, who rely on higher-priced alternative consulting services to drive revenue and consultant compensation.

Whether PE-owned or “independent,” the economic incentives all point in the same direction: Push pensions and retirement plans into higher-fee private equity and private credit—regardless of long-term risk to beneficiaries.

PE-Owned Consultants: Conflict at the Core

NEPC – Now indirectly PE-controlled

In 2025, Hightower Holding acquired a majority stake in NEPC. Hightower is itself majority-owned by private equity firm Thomas H. Lee Partners.

This means NEPC—long positioned as a “fiduciary-only” advisor—is now part of a private-equity-backed distribution platform.

Wilshire Advisors – Apollo’s footprint via Motive & CC Capital

Wilshire was taken private by Motive Partners and CC Capital, whose leadership and capital partners maintain deep ties to Apollo and the private markets ecosystem.

Wilshire has since pivoted aggressively toward alternatives advisory and OCIO mandates.

Russell Investments

Owned by TA Associates (majority) and Reverence Capital Partners, Russell is one of the largest OCIO platforms in the world. It profits directly when clients allocate more to alternatives under its discretionary management.

SageView Advisory Group (Aquiline)

For several years, private equity firm Aquiline Capital Partners held a controlling stake in SageView. Aquiline’s strategy: consolidate RIAs and drive asset growth into high-margin private-market solutions.

In short: When the owners of a consultant profit from private equity, the advice will inevitably steer clients toward private equity. Angeles Investment Advisors owned by PE firm Levine Leichtman Capital Partners. Prime Bucholz has been in minority partnerships with PE over the years.

Even consultants not owned by private equity have public shareholders pushing them toward higher-margin advisory services—namely private equity, private credit, and OCIO.

Mercer (owned by Marsh & McLennan)

Mercer operates one of the largest:

OCIO businesses in the world

Proprietary private equity funds-of-funds

Alternative investment research and distribution groups Mercer Alternatives bought Pavillion from PE firm TriWest Capital Partners in 2018, and still influences platform.

Mercer earns much higher fees for:

Private markets due diligence

Access to Mercer-managed PE vehicles

OCIO discretionary mandates

Marsh & McLennan’s investor calls make it clear: alternatives and OCIO growth drive shareholder value.

Aon

Aon aggressively markets:

Aon Private Markets

Aon Private Credit solutions

Aon OCIO

Aon’s 10-K filings explicitly list “delegated investment management” and private markets as key revenue drivers.

WTW (Willis Towers Watson)

WTW operates its own private equity platform:

WTW Private Equity Solutions

Commingled alternative funds

Infrastructure/real asset vehicles

WTW extracts multiple layers of fees when a pension allocates to alternatives through their platform.

Conclusion: Mercer, Aon, and WTW have financial obligations to public shareholders that directly incentivize recommending higher-fee private equity allocations. Rocaton was bought by Goldman Sachs a firm deeply embedded in private equity

This is the category most trustees and regulators mistakenly assume is “independent.” But employee-owned consultants still have major conflicts of interest tied to private equity fee structures.

Callan – Pay-to-Play Through Callan College

Callan promotes itself as independent and employee-owned. Yet:

Callan College allows asset managers—including private equity firms—to pay for access to plan sponsors.

Callan charges premium fees for alternatives consulting.

This creates a baked-in incentive to recommend private equity.

Meketa – Higher Fees for Private Markets

Meketa earns:

Standard fees for public markets consulting

Much higher fees for private equity, private credit, and hedge fund oversight

Plus, Meketa markets itself as a leader in private markets advisory, turning private equity consulting into a profit engine.

Charge materially higher fees for alternatives consulting

Promote themselves as experts in private markets

Benefit through staff growth and enhanced margins when clients increase private equity allocations

Even without PE owners, the internal compensation systems reward consultants who grow alternatives business. Others with substantial conflicts around PE include CEM, Global Governance Advisors, and Funston.

The Industry-Wide Conflict: Alternatives = Higher Fees

Across all ownership structures, the economic truth is the same:

Higher consulting fees; pay-to-play structures; prestige and internal incentives

APPENDIX

How Consultants Use Smoothed Returns to Justify Overallocations to Private Equity and Private Credit

Summary

Pension consultants systematically overallocate to private equity and private credit not because these assets demonstrably improve risk-adjusted outcomes, but because smoothed, appraisal-based return data mechanically overstates returns and understates risk in asset-allocation models. This distortion aligns with consultants’ economic conflicts and effectively turns asset-allocation modeling into a distribution mechanism for high-fee private assets.

1. Smoothed Returns Are a Known, Documented Problem

Illiquid private assets do not trade continuously and are typically valued using appraisals, models, or manager-supplied marks. This produces stale and artificially smoothed return series.

The CFA Institute (2025) explicitly warns that analysts must test for serial correlation and states that analysts “need to unsmooth the returns to get a more accurate representation of the risk and return characteristics of the asset class.”

Failure to unsmooth causes:

Understated standard deviation (volatility)

Artificially low correlation to public markets

Inflated Sharpe ratios

Illusory diversification benefits

This is not controversial; it is widely accepted in the academic and professional literature.

2. Optimization Models Convert Smoothing into Overallocation

Consultants then feed these distorted inputs into:

mean-variance optimization,

risk-parity frameworks, or

efficient frontier analyses.

When an asset shows:

high historical returns,

low reported volatility, and

low correlation,

optimization must recommend a larger allocation. The result is mathematically predetermined.

In other words, the model is not discovering diversification—it is laundering volatility.

3. Academic Evidence Confirms the Distortion

The 2019 SSRN paper “Unsmoothing Returns of Illiquid Assets” (Couts, Gonçalves, and Rossi) demonstrates that commonly used unsmoothing techniques are often inadequate and that true risk exposures—especially market beta and downside risk—are materially higher than reported.

Once proper unsmoothing is applied:

correlations to public equities rise,

volatility increases,

and much of the apparent alpha disappears.

This finding directly undermines consultant claims that private equity and private credit offer persistent, low-risk diversification benefits.

4. Why This Serves Consultant Conflicts

As documented in How America’s Largest Pension Consultants Became the Distribution Arm for Private Equity, consultants often have:

ownership ties to private-market platforms,

revenue relationships with private managers,

internal compensation incentives linked to alternatives adoption.

Smoothed returns provide the technical justification for conflicted recommendations. They allow consultants to present sales outcomes as fiduciary analytics.

This same logic applies to private credit, where appraisal-based pricing and delayed loss recognition further suppress volatility and correlation—despite operating in highly competitive credit markets where true excess returns are measured in basis points.

5. Fiduciary Implications

Asset-allocation decisions based on smoothed private-market returns:

overstate expected returns,

understate portfolio risk,

misrepresent diversification benefits,

and systematically bias portfolios toward high-fee private assets.

From a fiduciary perspective, an allocation recommendation that collapses once returns are properly unsmoothed is not prudent—it is misleading.

6. Minimum Disclosures Fiduciaries Should Demand

Any consultant recommending private equity or private credit should be required to provide:

Serial-correlation diagnostics on private-asset returns

Full disclosure of unsmoothing methodology and parameters

Asset-allocation results before and after unsmoothing

Changes in volatility, correlation, and beta post-unsmoothing

A clear explanation of how much of the recommended allocation depends solely on smoothed data

Absent these disclosures, claims of diversification and superior risk-adjusted returns lack credibility.

Zweig is right: Target Date CITs are black boxes. Participants are flying blind. Even fiduciaries often have no idea what they’re buying.

But here’s the deeper truth Zweig could only gesture toward:

State-regulated Collective Investment Trusts (CITs) are the primary mechanism Wall Street now uses to hide high-risk, high-fee products inside 401(k) plans — including Private Equity, annuities, structured credit, and even crypto.

And the industry is now lobbying Congress to expand these opaque products even further — through the INVEST Act, which would open the door for CITs in 403(b) plans, especially for teachers and nonprofit workers.

This is not investor protection. This is a massive subsidy and legal shield for Private Equity and insurers who have already hijacked the Target Date market.

Below is how Zweig’s reporting validates — and amplifies — the very warnings I’ve been documenting for years.

1. Zweig Exposed the Key Weakness of TDF CITs: Zero Transparency

Zweig’s article highlights what most participants do not know:

CIT TDFs do not file SEC prospectuses

CITs provide no daily portfolio holdings

CITs are regulated only by weak state trust departments, not the SEC

CITs routinely change allocations without public notice

CITs often use opaque pricing, smoothing, and valuation methods

Zweig showed the symptoms. But he did not go into the deeper pathology:

The entire CIT TDF ecosystem is built to avoid ERISA and avoid SEC oversight.

It is no coincidence TDF managers moved from mutual funds to CITs. They didn’t do it to save participants fees. They did it to avoid public scrutiny and to create a regulatory gray zone where anything can be hidden.

2. Weak State CIT Oversight Enables Hidden Private Equity, Annuities, and Crypto

As my research has documented:

CITs can legally contain:

Private Equity and Venture Capital

Private Credit / Direct Lending

Insurance annuity contracts

Structured products

Commodities

Crypto ETFs or crypto derivatives

Offshore vehicles

Securitized real estate

High-fee alternative managers

Use excessive leverage

None of this would be allowed inside an SEC-registered mutual fund without substantial disclosure.

Zweig asked the right question — “Do you know what’s inside your 401(k)?” But the deeper answer is:

You don’t know. And you’re not supposed to know. CITs are built specifically so you cannot know.

Even the Department of Labor cannot easily assess CIT risks because the data is not reported to them.

Any Target Date Fund run by a party-in-interest is vulnerable to a prohibited transaction lawsuit that cannot be dismissed at the pleading stage.

This is because:

Compensation exists

The CIT is proprietary or affiliated

The 5500 filings show the affiliation

§406 violations are strict liability — no intent required

And Zweig just gave the public the roadmap.

4. 5500 Forms Make It Easy to Identify Party-in-Interest TDFs

Zweig showed investors are unaware of what is inside their 401(k)s. But what he didn’t say is that lawyers and fiduciaries and even participants can easily identify party-in-interest relationships by checking:

Schedule C (service providers)

Schedule D (CCT/CIT holdings)

Trustee and custodian identities

Indirect compensation disclosures

Affiliated service provider names

This allows plaintiffs to identify:

TDFs run by the recordkeeper

CITs operated by plan consultants

CITs relying on affiliates for valuation services

Platforms that receive crypto pay-to-play or revenue-sharing

Spread-based GICs embedded in CIT “fixed income”

Wherever a TDF manager is also:

the recordkeeper,

the broker-dealer (BrokerageLink),

the consultant/advisor,

the custodian,

or the CIT trustee,

a prohibited transaction theory is not only viable — it is almost guaranteed.

5. Wall Street Is Now Trying to Change ERISA Rather Than Comply With It

Zweig highlights how confusing and opaque CITs have become.

If Private Equity, annuities, and crypto cannot legally be placed inside Target Date CITs under ERISA today, change ERISA so they can.

Congress is being used to rubber-stamp what would otherwise be:

clear party-in-interest violations,

clear §406 prohibited transactions,

and clear breaches of loyalty and prudence.

However, Cunningham v. Cornell was a 9-0 Supreme Court decision showing that even the most Wall Street friendly judges have refused to destroy ERISA protections of DC plan.

6. Wall Street Changing laws to allow Target DATE CITs in non-ERISA plans

Zweig’s findings strengthen four major litigation arguments:

1. CIT opacity = fiduciary breach per Tibble v. Edison

Fiduciaries cannot prudently monitor an investment whose holdings are secret.

2. CITs operated by a plan’s own service provider = prohibited transaction (§406)

Zweig just provided mainstream confirmation that these relationships are common.

3. Hidden alternatives (PE, annuities, crypto) = breach of duty of loyalty

Fiduciaries who cannot see risks cannot act in participants’ best interest.

4. CITs conceal revenue-sharing and indirect compensation = §406(b)(3) violation

Zweig’s discussion of hidden fees matches precisely what I’ve shown in multiple ERISA analyses.

Conclusion: The WSJ Just Confirmed What I’ve Warned for Years — But the Real CIT Corruption Is Still Hidden

Jason Zweig’s reporting is essential. But it is only the beginning.

CIT corruption runs far deeper:

Hidden Private Equity allocations

Hidden annuity spread profits

Hidden crypto exposure through derivatives and brokerage windows

Hidden trustee wrap fees

Hidden sub-advisor platform payments

Hidden GIC spread extraction

Hidden recordkeeper revenue-sharing

The WSJ piece has now validated what fiduciary experts and whistleblowers have documented for years:

Target Date CITs are the most dangerous, opaque, conflict-ridden investment vehicles in the 401(k) and 403(b) system — and they are at the core of modern ERISA prohibited transactions.

Zweig opened the door. It’s now time for litigators, fiduciaries, regulators, and Congress to walk through it.

Appendix: Why “Fee Disclosure Parity” Claims by State-Regulated CIT Trustees Miss the Fiduciary Point

A. The Great Gray Statement: Technically Accurate, Fiduciarily Irrelevant

I wanted to test my theories on CITs. A consultant and I were discussing and he decided to see what Great Grays response would be. He recently shared the following statement from Great Gray Trust, the largest trustee and promoter of state-regulated Collective Investment Trusts (CITs): who is owned by the Private Equity firm Madison Dearborn.

“The OCC has regulations specific to CITs (Regulation 9)… and a couple of states cross-reference or incorporate those regulations… While Great Gray has generally followed those regulations… OCC regulations do not have any specific disclosure requirements regarding CIT fees and expenses. Instead, DOL Rule 404a-5 dictates what must be disclosed… Therefore, it is our view that there should be no distinction between the fees and expenses required to be disclosed for a mutual fund or a CIT… Any attempt to hide fees would be inconsistent with the DOL rule.”

This statement is not blatantly false—but it is misdirection, and from a fiduciary and prohibited-transaction perspective, it is largely irrelevant.

The issue with state-regulated CITs is not whether a standardized fee table is technically disclosed. The issue is whether the underlying assets, valuation methods, revenue flows, and conflicts are capable of being truthfully and reliably disclosed at all.

That is precisely why annuities, private equity, private credit, and crypto are prohibited from mutual funds—and why their migration into state-regulated CITs is a regulatory end-run around ERISA.

B. Why Mutual Funds Prohibit Annuities, Private Equity, and Crypto

Mutual funds are subject to the Investment Company Act of 1940, SEC valuation rules, daily NAV requirements, and independent board oversight. These regimes do not permit assets whose pricing, fees, or performance are inherently opaque or manipulable.

As a result:

Annuities are excluded because spread profits, crediting rates, and insurer balance-sheet economics cannot be independently verified.

Private equity and private credit are excluded because non-market valuations allow fee and performance manipulation.

Crypto is excluded because custody, pricing, liquidity, and auditability are unreliable.

The prohibition is structural, not disclosure-based. The SEC does not say, “You may include these assets if you disclose them better.” It says, you may not include them at all.

That distinction is fatal to Great Gray’s argument.

C. Why OCC Regulation 9 Is a Red Herring

Great Gray correctly notes that OCC Regulation 9 governs national-bank-sponsored CITs and does not impose detailed participant-level disclosure requirements.